Golden Age: Container shipping’s post-covid boom continues

2024 set to be a record-breaking year as orders, deliveries and charter rates soar

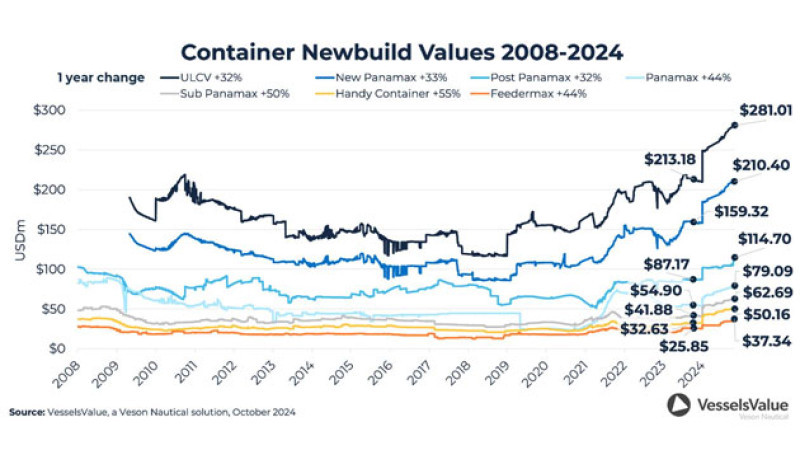

Values for Container newbuildings are currently at an all-time high. For example, New Panamax

newbuilding values for vessels of 15,000 TEU have continued to rise since the start of the year

and are currently at USD 210.50 mil, compared to USD 158.52 mil this time last year, this is an

increase of c.33% year-on-year. In the Post Panamax sector of 7,000 TEU, values surpassed the

previous record set in 2010 earlier this year and have continued to rise from that point.

At the moment, New Panamax newbuildings are valued at USD 114.7 mil, an increase of c.32%

year-on-year from USD 87.03 mil.

Newbuilding costs in this sector have risen due to increased demand, limited yard availability,

climbing material costs and competition from other ship types occupying available spaces.

So far this year, Container newbuilding orders are up by c. 52% year-on-year with 254 new

contracts placed this year, compared to 167 in the first 10 months of 2023. The majority of

orders placed this year were in the New Panamax sector, accounting for c.41%, followed by Post

Panamaxes with a share of c.27 and in third place, ULCVs with c.22%.

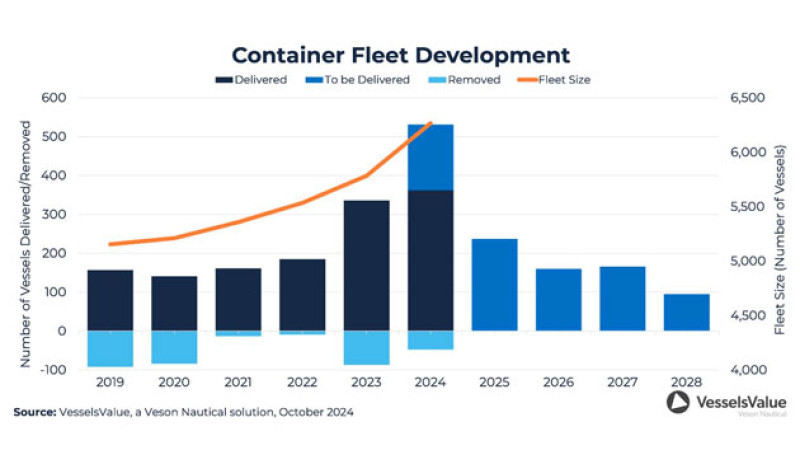

In addition, there have been a considerable amount of newly delivered Container vessels

entering the fleet over the last few years, thanks to the post covid Container boom. 2024,

represents a record year for new Container vessels entering the market, so far this year there

have been 362 vessels delivered, with a further 169 set to be delivered in the last few months of

the year.

At the same time, due to the firm earnings this year, removals remain low with just 48 Container

ships sent for demolition, a fall of c.45% year-on-year. The average age of the total Container

fleet is 12 years of age, and with older vessels in abundant supply as a result of the previous

ordering boom of the 2000’s there is some potential to scrap, should earnings fall once again.

Although 2023 saw Container earnings dip from the highs of 2021-2022, as the market returned

to normal following the boom period of the covid lockdowns. Since the start of 2024, Container

earnings have firmed once again and are currently up year-on-year across all sectors. This is

due to the additional ton mile demand which has arisen as a result of the hostilities in the Red

Sea, which has forced vessels to travel longer distances around the Cape of Good Hope.

There are also several other factors contributing to the elevated TC rates at the moment such as

GRI’s (General Rate Increases) set to go live from the middle of November and along with a

strike in Canada and strong volumes traded. In the Post Panamax sector, earnings are currently

double the figure seen this time last year.

One year time charter rates for Post Panamaxes have been hovering around the 72,000 USD/Day

mark since July, this is an increase of 100% from the same time last year, where rates were

around 36,000 USD/Day.

Notable recent newbuilding contracts include 10 x New Panamax Container vessels of 16,000

TEU ordered by Moller Maersk, scheduled to be built at Hanwha Ocean and delivered in 2027,

contracted for USD 209.58 mil each, VV value USD 225.51 mil each. Also, 6 x New Panamax

Container ships of 13,600 TEU and 10 x ULCVs of 16,000 TEU, ordered by Seaspan, scheduled

to be built at Hudong Zhonghua and delivered between 2027-29.

Author: Rebecca Galanopoulos