Market Outlook - End Q2 2024 Forecast Values

Chinese economy's recovery, elevated interest rates and ongoing political tensions add to an atmosphere of uncertainty

Overview

There are several elements of unpredictability affecting our shipping market forecasts for the second quarter of 2024. The Chinese economy's recovery currently teeters on instability, casting a shadow of uncertainty over the industry due to China's pivotal role as a major demand driver. Elevated interest rates in Western economies heighten the risk of a severe downturn, potentially stalling prospective growth. Ongoing geopolitical tensions, coupled with related repercussions and sanctions, add to an atmosphere of uncertainty; any notable escalation or de-escalation in these conflicts could profoundly affect the broader economic trajectory. And lastly, the potential for disruption in the Panama Canal and Suez Canal, influenced by both natural occurrences and the unpredictable nature of certain military groups, is injecting an additional element of instability into the economic landscape.

Here’s a breakdown of how this uncertainty could play out across tankers, bulkers, containers, and gas industries.

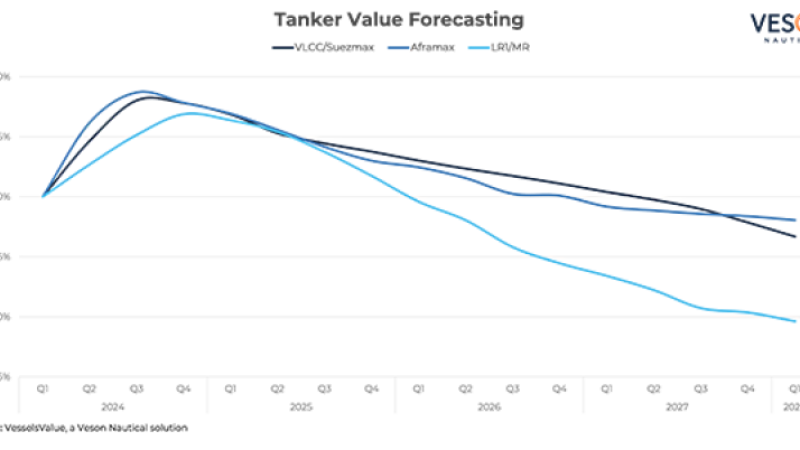

Tankers

• Volatility in rates and expectations will continue with movements in the oil price, Russian volume developments, OPEC+ decisions, and member compliance, as well as China’s ability to maintain economic growth and high crude imports and refinery runs.

• Uncertainty surrounding the extent to which Russian production and exports will be affected by sanctions imposed by authorities or via voluntary measures taken by traders, shipowners, insurance companies, and oil companies will continue to influence activity in the foreseeable future.

• After picking up in 2023, Tanker ordering has continued this past quarter. The total DWT ordered so far is more than twice the amount ordered during the first quarter of 2023, despite high newbuilding prices.

• Tonne-mile demand expectations in 2024 and beyond remain strong in our current Base Case, following negative developments in both 2020 and 2021 for the total Tanker market, including both crude and product carriers.

• During 2024, tonne-mile demand will be boosted by the impact of vessels avoiding the Red Sea, a development which could be reversed during the next couple of years of our forecast period.

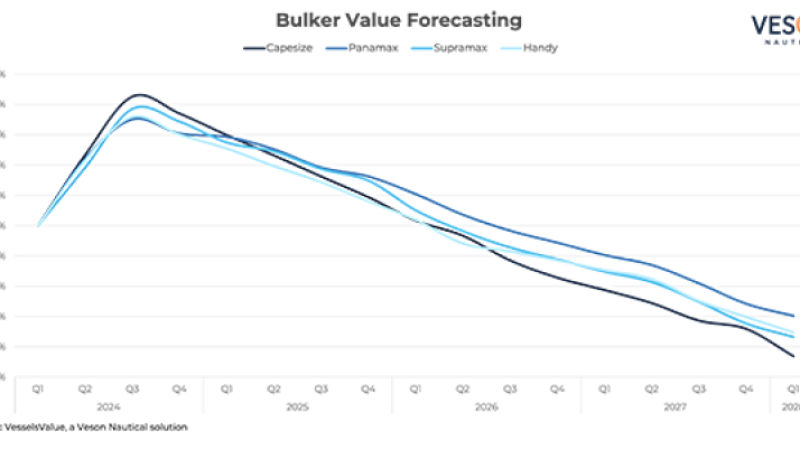

Bulkers

• Modest growth in demand is expected to surpass low growth in supply, paving the way for a fundamentally strong market balance.

• The current canal disruptions and the consequent rerouting of vessels is adding an additional layer of upside in the near term as tonne-miles are significantly affected.

• China is investing heavily in green energy and has become a leading producer of new energy vehicles and solar panels. This trend is expected to continue, which will support domestic steel demand.

• The anticipated opening of the Simandou iron ore mine in Guinea in 2025 is poised to reshape the dynamics of the iron ore trade and will likely increase iron ore tonne-miles due to the longer sailing distances.

• Coal demand is expected to peak this year but is predicted to remain firm in the foreseeable future.

• A low orderbook and hesitancy to invest in new vessels amid fuel-related uncertainties has restricted the upcoming deliveries in the Bulker sector. This has created a favorable supply situation for shipowners, as net fleet growth is limited.

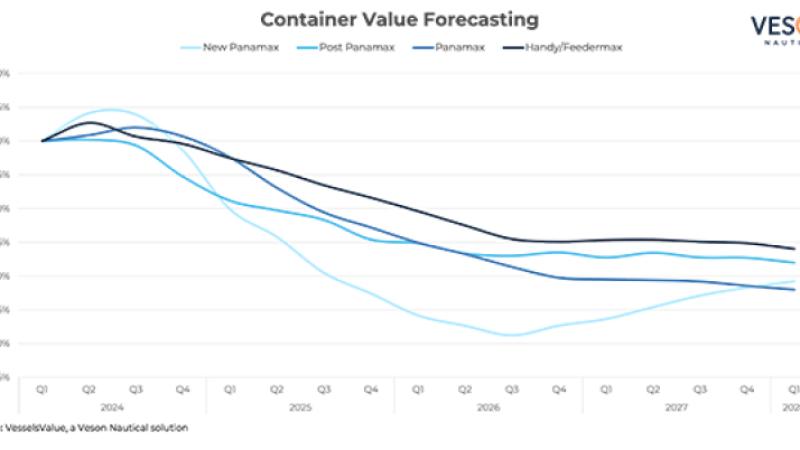

Containers

• Our current analysis points to demand growth of 3.1% yearly average over the period from 2024-2027, with a forecasted growth of 2.4% for 2024.

• In conjunction with easing congestion, rates have come down sharply and are expected to bottom out between the second half of 2024 and the first half of 2025, before rising somewhat as the pains of returning to normal abate. Despite the non-fundamental increase in freight rates in the past months, we believe rates will come under pressure and continue to decline in 2024.

• With almost 9 mil TEU’s entering the market over the next couple of years, we expect a supply surplus. Looking at the orderbook, dual fuel vessels account for c.45% in terms of vessels and even more in terms of TEUs, indicating liners are well underway in the green transition, with LNG and Methanol being the preferable solution. The orderbook is still significant at c.27% of the fleet at the beginning of 2024.

• Scrapping activity has remained muted with 0.13 mil TEU’s in 2023, but this is expected to increase going forward. With the EU ETS being live and a general tightening of CO2 emissions regulations, we anticipate that operating elderly, non-eco vessels will become increasingly costly.

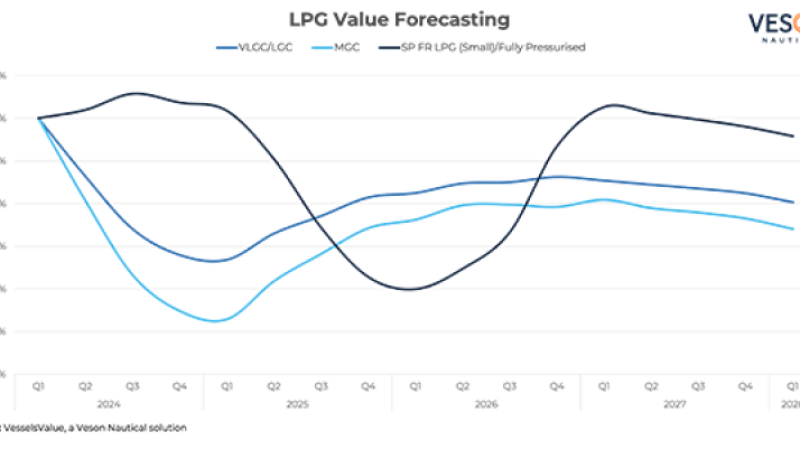

Gas

• In the US, we expect LPG production to grow at a slower speed than previous years and forecast a growth of 2.1% in 2024. Exports will also grow at a moderate pace in 2024 due to the latest terminal expansion in the fourth quarter of 2023.

• VLACs have been a hot topic lately, with several vessels expected to be delivered in 2026 and 2027. However, we do not expect the new vessels to load ammonia in their first few years, but rather LPG until the ongoing blue and green ammonia projects reach sufficient volumes.

• Earnings are forecasted to see a correction throughout 2024 as US production growth is expected to be modest and domestic consumption is likely to increase.

• The stress on transits through the Panama Canal is likely to see large seasonal variations, with the recent draught in the Gatun Lakes as something that could substantially impact VLGC transits in the following years. However, we expect an increase in daily transits for 2024 as the water level projections are improving according to Panama Canal Authority.

• Asian demand for LPG is forecasted to see slight growth in 2024 for PDH plants and domestic consumption as economic growth is moderate and oversupply is still a concern. We forecast a continuation of the current trade pattern in the ammonia market, with increasing demand in Asia.

• In the petrochemical gas trades, US ethylene is expected to continue to ship to Asia and Europe on price competitiveness.